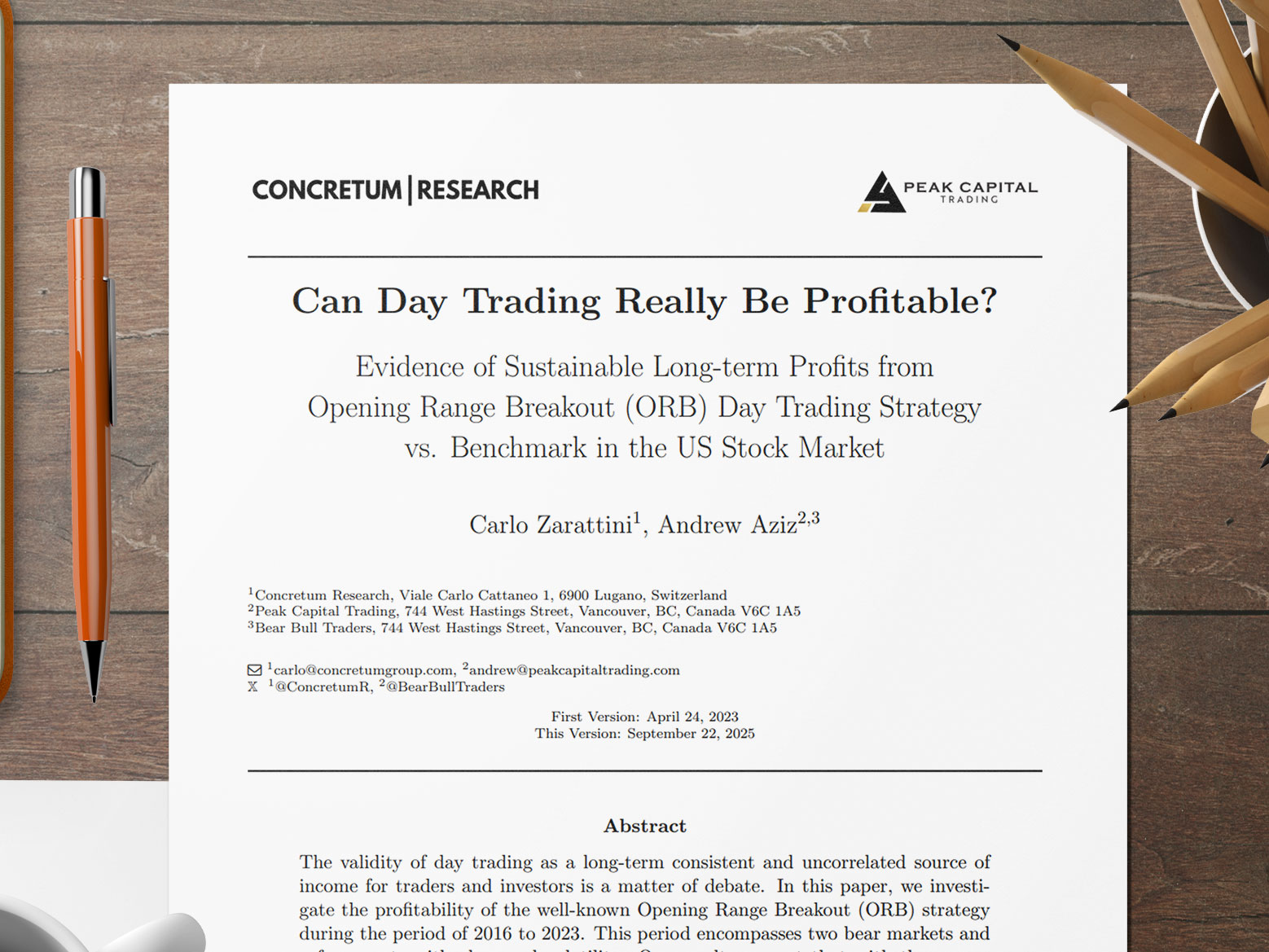

Can Day Trading Really Be Profitable?

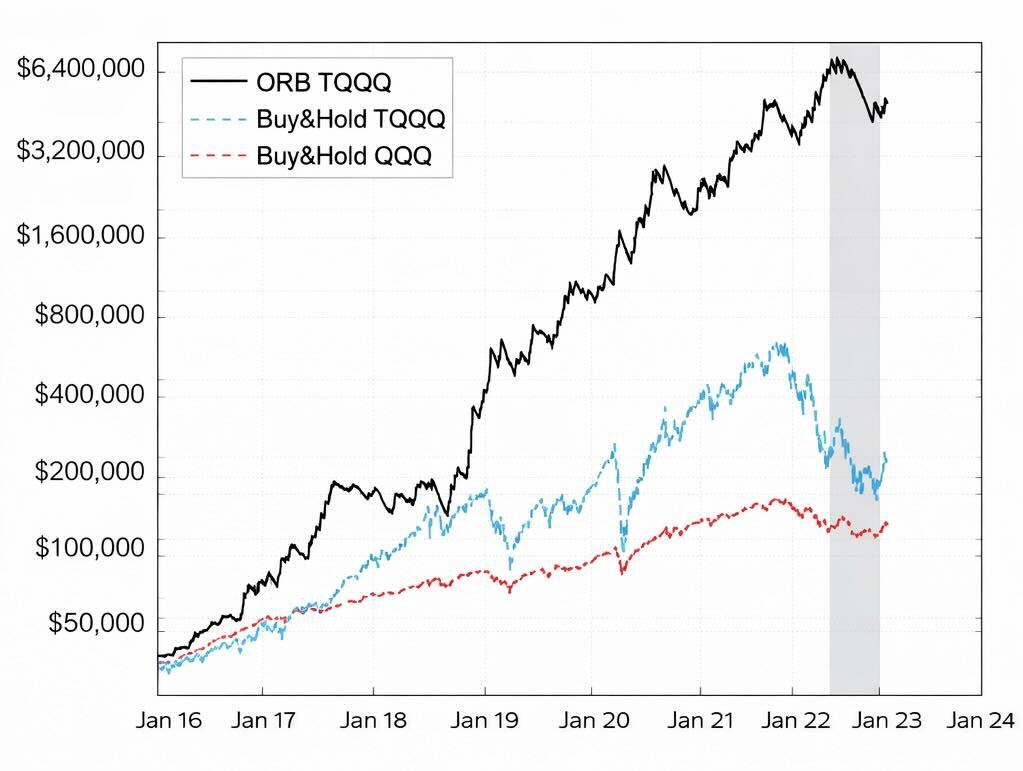

Study of Opening Range Breakout strategy vs passive benchmarks showing sustainable long-term profits.

Read Paper →Empirical academic research by Andrew Aziz and finance collaborators analyzing disciplined systematic strategies vs passive benchmarks.

Andrew Aziz — Live Presentations Worldwide.

Study of Opening Range Breakout strategy vs passive benchmarks showing sustainable long-term profits.

Read Paper →

Analysis of VWAP-based strategy performance on leveraged products from 2018–2023.

Read Paper →

Stocks in Play ORB research showing net performance above 1,600% with high catalysts and volume.

Read Paper →

Quantitative results for an intraday momentum strategy on SPY with Sharpe ratios above 1.3.

Read Paper →

Study on volatility strategies using VIX ETNs with low correlation to equities and disciplined execution.

Read Paper →

Investigation into how Martingale betting systems can mislead through statistical manipulation.

Read Paper →

Our peer-reviewed studies show that a disciplined Opening Range Breakout strategy on leveraged instruments like TQQQ has dramatically outperformed passive buy-and-hold benchmarks over an eight-year period, while carrying lower drawdown risk during major market dislocations.

This isn’t a backtest cherry-picked from a single year. It’s rigorous, published academic work. The kind of edge that Bear Bull Traders is built on.

Read the Full Study →