The Housing Market Horror Continues

Dear Traders,

I apologize for not trading on Thursday as I took the day off to relax. Today, market volatility continued with a significant gap up in the market and we traded notable breakouts on $NVDA, $TSLA, and $TQQQ.

Watch my recap to see how I successfully traded these names. As I write this letter, the market is giving up all the early gains of the morning session. Today marks the end of the quarter, and investors are pricing in and digesting higher interest rates for a longer period, as well as inflation and personal income/spending numbers that were released today.

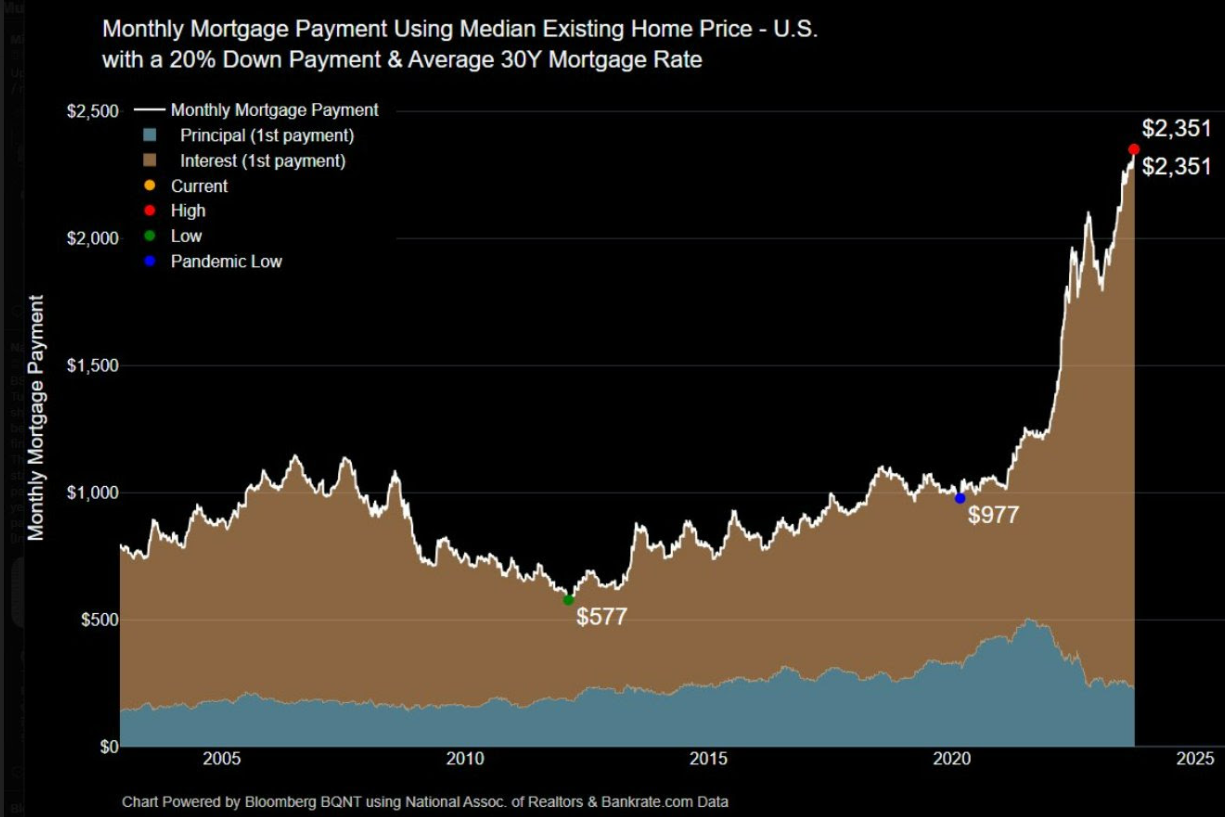

Everybody has been extensively discussing the troubles in the U.S. housing market over the last eighteen months. Below is a chart that tracks an “average” home purchase over the last 20+ years. It calculates the monthly mortgage payment using median existing home prices, assuming a 20% down payment and average 30-year mortgage rates.

After the 2008 financial crisis, low home prices and interest rates were significant tailwinds for keeping this value in a reasonable range. But during the pandemic, there was an explosion in demand for homes, driving up prices. Then the Fed raised interest rates at their fastest pace ever, causing a major double-whammy for homebuyers.

The result? The average monthly mortgage payment is up 141% from its pandemic low of $977. That’s the type of increase that previously took years to occur, and yet it’s happened in about three years, as shown by the parabolic rise in this chart since then.

For those who already own a home and are locked in at low rates, this dramatically boosts their net worth. However, for Millennials and Gen Z looking to purchase their first home, start families, and have kids, they’re facing the worst affordability in decades.

This chart is a stark reminder of the current U.S. housing environment and the potential economic impact of those who want to form households but can’t do so at current prices. The current headwinds will unlikely improve until a financial shock or economic downturn forces people to sell their homes.

Barring builders creating a lot more new construction, that’s about the only thing that will improve existing inventory levels, as current owners have little incentive to move. In most parts of the USA, it’s more affordable to rent than buy at current prices, especially when considering the many other costs associated with owning, like property taxes, insurance, repairs, etc.

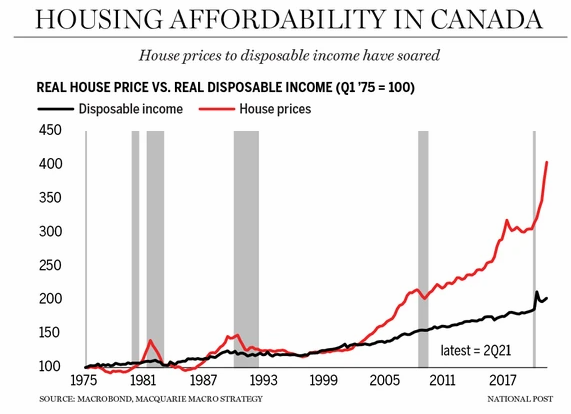

In Canada, where approximately 1.2 million immigrants are accepted each year, the situation is even more challenging. Cities and municipalities cannot accommodate such an influx of people, and as more people enter major cities like Vancouver, Montreal, or Toronto, housing prices become increasingly challenging.

In MoneyShow Toronto, we learned about the challenges ahead in the affordable housing market from notable speakers, such as the head of a major Canadian bank, the Canadian Imperial Bank of Commerce (CIBC). They mentioned that in their meetings with government officials, they have already expressed concerns that the current situation is unstable and could lead to social unrest.

Let’s see how the market unfolds. The rates are unlikely to come down lower unless inflation is back on track to the 2% target set by central banks, and unemployment ticks higher toward 4%-4.5%.

We are witnessing interesting times. As Federal Reserve Chairman Jerome Powell said in one of his meetings, the pandemic revealed how little we know about inflation and how resilient the economy is.

To your success,

Andrew